Written By WWW.SSA.GOV

At Social Security, we’re often asked, “What’s the best age to start receiving retirement benefits?” The answer is that there’s not a single “best age” for everyone and, ultimately, it’s your choice. The most important thing is to make an informed decision. Base your decision about when to apply for benefits on your individual and family circumstances. We hope the following information will help you understand how Social Security fits into your retirement decision.

Your decision is a personal one

Would it be better for you to start getting benefits early with a smaller monthly amount for more years, or wait for a larger monthly payment over a shorter timeframe? The answer is personal and depends on several factors, such as your current cash needs, your current health, and family longevity. Also, consider if you plan to work in retirement and if you have other sources of retirement income. You must also study your future financial needs and obligations, and calculate your future Social Security benefit. We hope you’ll weigh all the facts carefully before making the crucial decision about when to begin receiving Social Security benefits. This decision affects the monthly benefit you will receive for the rest of your life, and may affect benefit protection for your survivors.

Your monthly retirement benefit will be higher if you delay starting it

Your full retirement age varies based on the year you were born. You can visit www.ssa.gov/planners/ retire/retirechart.html to find your full retirement age. We calculate your basic Social Security benefit — the amount you would receive at your full retirement age — based on your lifetime earnings.

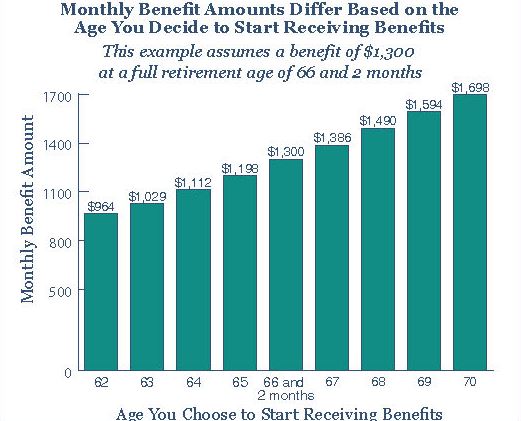

However, the actual amount you receive each month depends on when you start receiving benefits. You can start your retirement benefit at any point from age 62 up until age 70, and your benefit will be higher the longer you delay starting it. This adjustment is usually permanent: it sets the base for the benefits you’ll get for the rest of your life. You’ll get annual cost-of-living adjustments and, depending on your work history, may receive higher benefits if you continue to work. The following chart shows an example of how your monthly benefit increases if you delay when you start receiving benefits.

Let’s say you turn 62 in 2020, your full retirement age is 66 and 8 months, and your monthly benefit starting at full retirement age is $1,000. If you start getting benefits at age 62, we’ll reduce your monthly benefit 28.4 percent to $716 to account for the longer time you receive benefits. This decrease is usually permanent. If you choose to delay getting benefits until age 70, you would increase your monthly benefit to $1,266. This increase is the result of delayed retirement credits you earn for your decision to postpone receiving benefits past your full retirement age. The benefit at age 70 in this example is about 76 percent more than the benefit you would receive each month if you start getting benefits at age 62 — a difference of $550 each month.

Retirement may be longer than you think

When thinking about retirement, be sure to plan for the long term. Many of us will live much longer than the “average” retiree, and most women live longer than men. About one out of every three 65-year-olds today will live until at least age 90, SocialSecurity.gov and one out of seven will live until at least age 95. Social Security benefits, which last as long as you live, provide valuable protection against outliving savings and other sources of retirement income. Again, you’ll want to choose a retirement age based on your circumstances so you’ll have enough Social Security income to complement your other sources of retirement income.

Married couples have two lives to plan for

Your spouse may be eligible for a benefit based on your work record, and it’s important to consider Social Security protection for widowed spouses. After all, married couples at age 65 today would typically have at least a 50-50 chance that one member of the couple will live beyond age 90. If you are the higher earner, and you delay starting your retirement benefit, it will result in higher monthly benefits for the rest of your life and higher survivor protection for your spouse, if you die first. When you are receiving retirement benefits, your children can also be eligible for a benefit on your work record if they’re under age 18 or if they have a disability that began before age 22.

You can keep working

When you reach your full retirement age, you can work and earn as much as you want and still get your full Social Security benefit payment. If you’re younger than full retirement age and if your earnings exceed certain dollar amounts, some of your benefit payments during the year will be withheld. This doesn’t mean you must try to limit your earnings. If we withhold some of your benefits because you continue to work, we’ll pay you a higher monthly benefit when you reach your full retirement age. So, if you work and earn more than the exempt amount, it won’t, on average, decrease the total value of your lifetime benefits from Social Security — and can increase them. Here is how this works: When you reach full retirement age, we’ll recalculate your benefit to give you credit for months you didn’t get a benefit because of your earnings. In addition, as long as you continue to work and receive benefits, we’ll check your record every year to see whether the extra earnings will increase your monthly benefit. You can find more information about working after retirement on our website at www.ssa.gov/planners/retire/whileworking.html.

Don’t forget Medicare

If you plan to delay receiving benefits because you’re working, you’ll still need to sign up for Medicare three months before reaching age 65. If you don’t enroll in Medicare medical insurance or prescription drug coverage when you’re first eligible, it can be delayed, and you may have to pay a late enrollment penalty for as long as you have coverage. You can find more detailed information about Medicare on our website at www.socialsecurity.gov/benefits/medicare.

More resources

You can find more information to help you decide when to start receiving retirement benefits by using our benefits planners at www.socialsecurity.gov/ planners. If you have a my Social Security account, you can get your Social Security Statement to verify your earnings and use the Retirement Calculator. If you don’t have a my Social Security account, you can create one at www.socialsecurity.gov/myaccount or you can use our online Retirement Estimator at www.socialsecurity.gov/estimator. These tools provide retirement benefit estimates based on your actual earnings record. When you’re ready for benefits, you can also apply online at www.socialsecurity.gov/applyforbenefits. If you want more information about how your earnings affect your retirement benefits, read How Work Affects Your Benefits (Publication No. 05-10069). This pamphlet has the current annual and monthly earnings limits.

Contacting Social Security

The most convenient way to contact us from anywhere with any device is to visit www.socialsecurity.gov to get information and use basic services. We offer additional services when you create a secure online my Social Security account. Call us toll-free at 1-800-772-1213 or at 1-800-325-0778 (TTY) if you’re deaf or hard of hearing. We can answer your call from 7 a.m. to 7 p.m., weekdays. Or use our automated services via telephone, 24 hours a day. We look forward to serving you.